Disruptive Healthcare 11/29/2024 - Disruptive Peers a Bright Spot While Healthcare Lags Broader Market

Disruptive healthcare valuation, trends and analysis.

Healthcare Continues to Underperform:

Since the beginning of 2024, Healthcare as a sector has underperformed the broader market. The chart below takes the daily performance differences of the XLV and the S&P 500 then indexes that difference daily. This index shows the relative strength of the XLV versus the broader market and you can see that Healthcare has traded worse than the broader market for most of the year with a significant underperformance since the end of summer. Today, that index sits at a negative differential of 16.8 as shown in the chart below.

Are We Near a Relative Bottom for Healthcare?

Goldman Sachs created a chart to show what the XLV versus the S&P 500 looked like leading into and just after the 2016 election. So far this year looks a lot like 2016. In 2016 the relative weakness for the XLV bottomed in the months after the election then improved - although didn’t get back to even though the summer of 2017. We are hopeful that the bottom is in and the sector will trade better post-election.

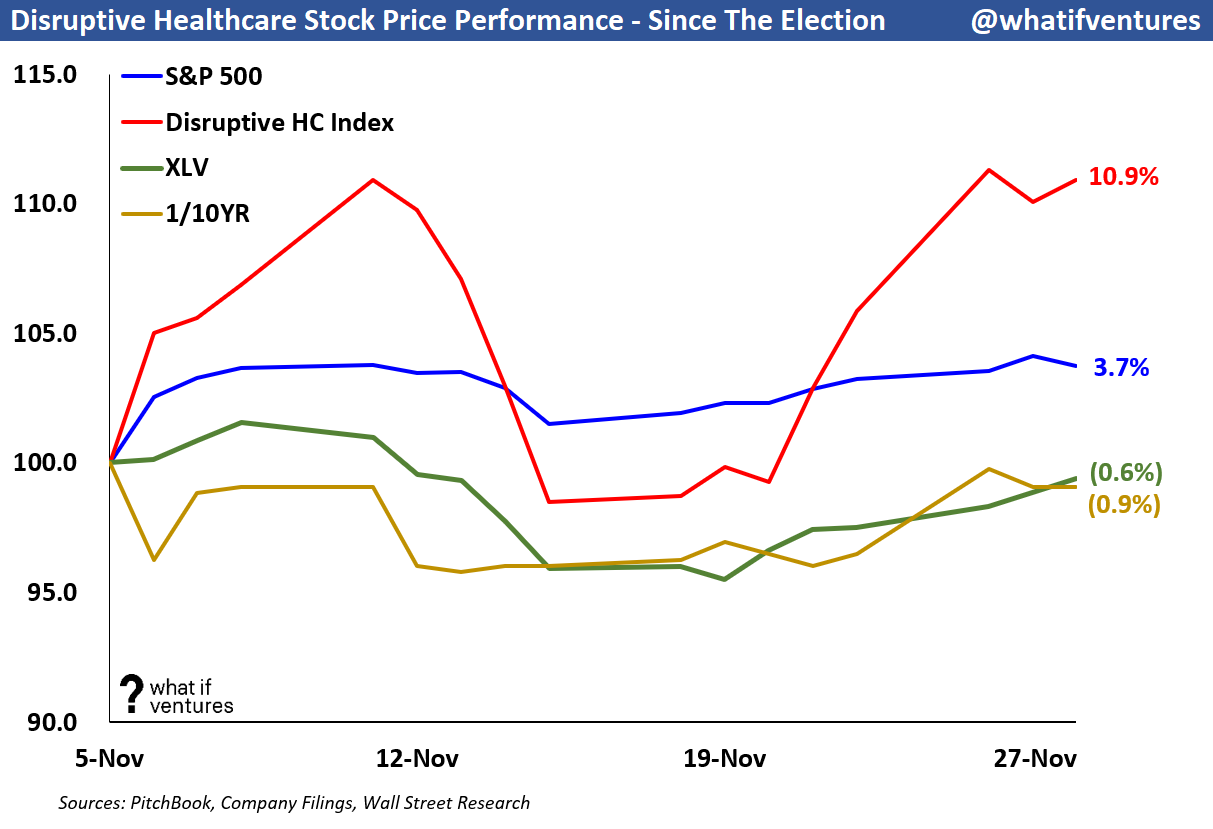

Disruptive Healthcare Peers Doing Better:

The bright spot in our opinion is the Disruptive Peer group that has outperformed the broader market and XLV since the election. This outperformance has allowed our peer group to almost catch up to the S&P 500 on a trailing 12-month basis as well.

Peer performance vs. broader market since the election:

Peer performance vs. broader market over the last 12 months:

As indicated via our indexed chart at the top of this note, the XLV is lagging the broader market and has been for most of this year. In this chart, you’ll see the green line (XLV) has lagged the blue line (S&P 500) for the last 12 months clearly.

However, in a positive signal to me as an early-stage healthcare investor, the Disruptive Peers have traded well lately, outpacing the Healthcare sector and closing the gap between the peers and the S&P 500 for the LTM period.

Stock Price Performance by Company:

Disruptive Healthcare Public Comps:

Turning to valuation, we’ve seen an improvement in NTM revenue multiples lately for our peers. Our Disruptive Healthcare peer group is currently trading at 3.7x 2025E revenue and 3.4x 2026E revenue.

Top 4 Revenue Multiples:

This top 4 group is a subset of the broader disruptive healthcare peer set. These 4 currently have the greatest EV / 2025 Revenue multiples of the broader group. These 4 companies as a group trade at 9.3x 2025E revenue versus the broader group at 3.7x. This group also boasts an average EBITDA margin of 36.8% on 2025E projections versus the broader group at 17.1% 2025E EBITDA margin.

Valuation — EV / NTM Revenue:

Mature healthcare comps are generally valued based on their earnings (see the broader comps at the bottom of this post). However, earlier stage businesses such as startups, and to an extent these younger, disruptive healthcare public companies often don’t have positive earnings yet or they may have positive earnings, but they haven’t reached the margin profile they will achieve upon maturity as a business. As a result, it’s harder to compare these companies on an apples-to-apples basis using EV to earnings. So, we use EV/NTM revenue to triangulate valuation for these companies and for startups in similar markets.

Summary of EV / NTM Revenue Valuation Stats:

5 Year Average: 6.5x

Today: 3.8x

Peak: 16.0x

Trough: 2.4x

Summary of top 4 EV / NTM Revenue Valuation Stats:

5 Year Average: 10.7x

Today: 9.5x

Peak: 21.9x

Trough: 5.5x

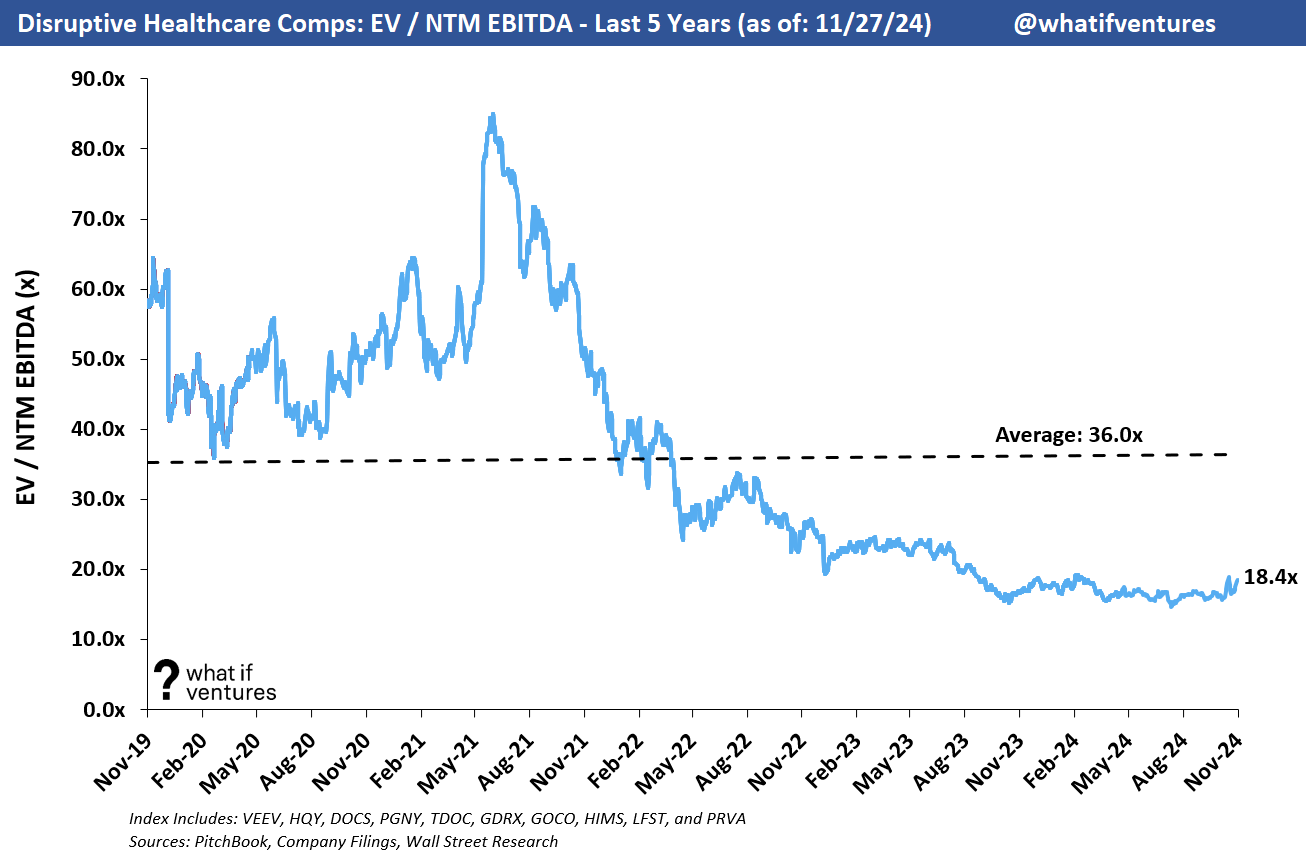

Valuation — EV / NTM EBITDA:

We were previously only looking at 8 companies from the perspective of EV/NTM EBITDA, but since Q1 earnings have reported, more analysts are projecting positive EBITDA in 2024 and beyond for more of the peers so we have expanded the index here to include 10 of the 16 companies. Based on what I’m seeing in equity research I think we will be adding a few names to this list soon as more of our peer group is starting to approach profitability.

To create an index, I only include the peers who have a substantial believable positive NTM EBITDA forecast based on the average of Wall Street equity research reports. The comps with barely positive EBITDA yield EBITDA multiples that aren’t realistic (so we consider them not meaningful “NM”).

The included companies are: VEEV, HQY, DOCS, PGNY, TDOC, GDRX, GOCO, HIMS, LFST, and PRVA. That’s not to say the other Companies won’t have positive EBITDA in 2024, but the multiples are relevant right now. Here’s how the chart looks.

Summary EV / NTM EBITDA Valuation Stats:

5 Year Average: 36.0x

Today: 18.4x

Peak: 85.0x

Trough: 14.7x

As these companies mature and begin to trade on EBITDA multiples or even P/E multiples (much like the hospital facilities and MCO peers) then this chart will tell us more. This is certainly a data point we can look at for profitable growth equity stage private companies. I’d expect those companies to be valued closer to the 5-year average or slightly lower. Some of that data in 2019 and 2020 is elevated because the EBITDA estimates back then were very small or barely positive for some of these companies driving an artificially high multiple that wasn’t driving valuation but rather was a dependent variable.

Broader Healthcare Comps as of 11/28/2024:

This newsletter is mostly focused on the disruptive healthcare comps and how their performance drives valuation for our private market portfolio at What If Ventures. However, we do keep a much broader set of comps that includes Healthcare Facilities and Managed Care Organizations.

^I realize this is too small to read, but if you double click on the image it should expand. Or you can just email me and I’ll send you the backup.

If you would like to receive weekly updates on this data and our outlook on the Disruptive Healthcare market, then please subscribe and share our work with a friend.

About What If Ventures — What If Ventures invests in mental health and digital health startups from seed stage to growth equity. To date, we have invested over $100mm into 82 (mostly) healthcare startups since January 2020. The firm is actively managed by Stephen Hays.

If you have questions about any of this analysis or want to collaborate with What If Ventures, please reach out via info@whatif.vc. We’d love to connect with entrepreneurs and investors in the space.

You can follow more of Stephen’s commentary on twitter here: @hazesyah